{kind=link}

This text is dropped at you by our sponsor, Empower. Empower Private Wealth, LLC (“EPW”) compensates Properly Saved Pockets for brand new leads. Properly Saved Pockets just isn’t an funding consumer of Private Capital Advisors Company or Empower Advisory Group, LLC.

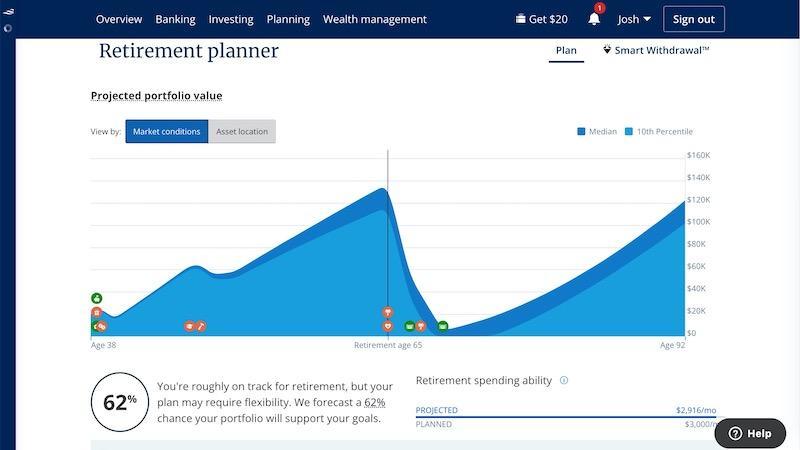

Figuring out in the event you’re saving sufficient for retirement is a query value asking repeatedly throughout your profession. Checking your present progress with a retirement planner is likely one of the simplest methods to check a number of eventualities to avoid wasting confidently.

Personalised Retirement Projections

Basic retirement financial savings suggestions, resembling investing 10% of your earnings in retirement accounts or saving 25 occasions your annual bills, are glorious beginning factors. Nonetheless, you lack a customized plan with a blanket strategy that may make you surprise in the event you’re heading in the right direction.

A number of years into my profession, I turned pissed off with following solely the fundamental recommendation as soon as I had a agency grasp on my fast bills and will focus extra intently on long-term objectives. Older colleagues encouraging me to get critical about retirement in my 20s was a further issue.

Empower presents a free retirement planner that I recurrently use to observe my funds. You possibly can enter a number of pre- and post-retirement objectives and regulate your retirement age to visualise your progress.

Take into account operating the next calculations via the planner:

- Earnings and bills: Run conditions with completely different earnings and expense quantities.

- Objectives: See how a lot it’s good to save for upcoming objectives and life-style modifications.

- Life occasions: Add notable moments resembling kids, weddings, and school.

- Retirement age: Discover early, on-time, and delayed goal retirement dates.

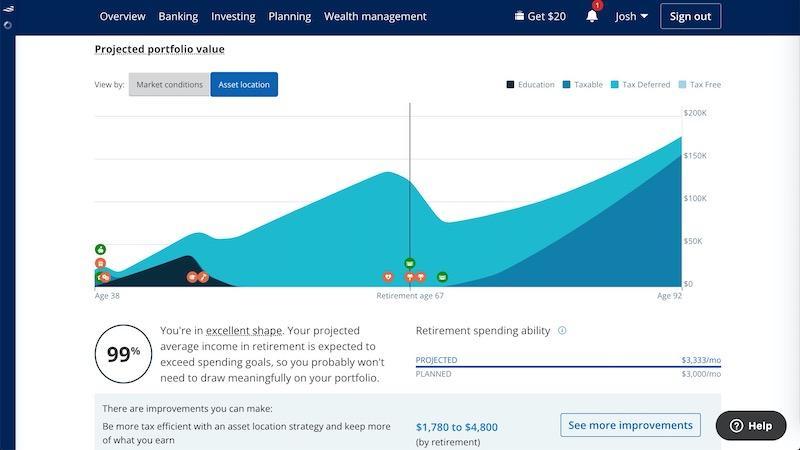

The calculator runs 5,000 Monte Carlo simulations to venture your retirement financial savings, Social Safety earnings, and funding asset allocation. You may also embrace the Dot Com or Nice Recession market drawdown patterns in your simulations to predicate your portfolio efficiency.

You will notice a chance of retirement success, your retirement spending capacity, and steered enhancements.

You’ll want to embrace all of your monetary accounts and earnings streams for an correct projection. As an illustration, you’ll want to listing pension and rental property earnings. You may also add one-time windfalls, resembling a house sale or inheritance.

Additional, I like that the planner makes state-specific tax calculations and permits you to edit your earnings tax bracket and inflation fee assumptions. A no-frills retirement calculator is much less more likely to supply these particulars.

Observe A number of Objectives

A sound monetary plan helps you afford near-term, mid-term, and long-term objectives. Life is a journey; including these targets permits you to see the entire story upfront. In consequence, you’re much less more likely to sacrifice milestones which are nonetheless years away or delay retirement.

Main purchases in your wishlist could embrace:

- Boat

- Basic automotive

- Funding Properties

- Hobbies

- Dwelling renovations or upgrades

- Alternative automobiles

- Journey

- Trip house

Should you’re like me, there are a number of occasions if you ask, “Can we afford this proper now?” It may be simple to focus virtually solely in your fast priorities and overlook about retirement nonetheless a long time away. Working the numbers provides confidence to your determination course of.

A written plan helps allocate your earnings on your pre-retirement objectives whereas persevering with to avoid wasting for retirement month-to-month. The retirement calculator’s chart additionally lets you see how the acquisition impacts your saving capacity and future nest egg stability.

Suppose you want digging deep into the information. In that case, you’ll be able to view a money move desk highlighting your beginning portfolio worth, yearly spending, and money financial savings quantities throughout your accumulation part and retirement years.

Plotting your present monetary ambitions with the one-time or ongoing expense quantity and motion date shows your estimated portfolio worth by age. You need to use the opposite Empower Retirement App options to observe your money move, real-time account balances, and extra.

Plan for the Sudden

Shock payments are inevitable, and boosting your emergency fund to cowl the associated fee is certainly one of a number of techniques to pursue. Often, you’ll be able to plan forward of time for bills like a roof alternative or new automotive tires with out understanding the exact date or greenback quantity.

Nonetheless, different conditions require your greatest estimate. You could have to pay for all the quantity out of pocket or cowl the distinction that insurance coverage doesn’t reimburse.

Utilizing your private circumstances and skilled analysis as a baseline, you must also put aside funds for the next:

- Funerals

- Job loss

- Medical payments

- Pet emergencies

- Storm-related house repairs

- Tax and insurance coverage will increase

- Utility repairs and alternative

- Premature car repairs

Relying in your budgeting model, sinking funds save cash for a particular objective. Identical to you could have a retirement fund, these devoted accounts forestall you from shedding your financial savings progress for different objectives.

If in case you have an eligible healthcare plan, a well being financial savings account (HSA) permits you to save for future medical bills with tax-deductible contributions and tax-free withdrawals. Your employer may supply tax-advantaged accounts that may handle sure prices throughout your working years so you’ll be able to allocate extra of your take-home pay in the direction of your internet value.

Periodically reviewing your insurance coverage insurance policies and deductibles can be sure that you’re adequately insured whereas minimizing your potential out-of-pocket bills.

Household Planning and Training

Updating your retirement plan and month-to-month bills as your family measurement grows and also you add extra dependents can be important for accuracy. As a father of 5, my spending and financial savings patterns have shifted through the years to set my kids up for monetary success.

Bills it would be best to plan for embrace:

- Dependent help (i.e., kids and getting older family members)

- Training

- Weddings

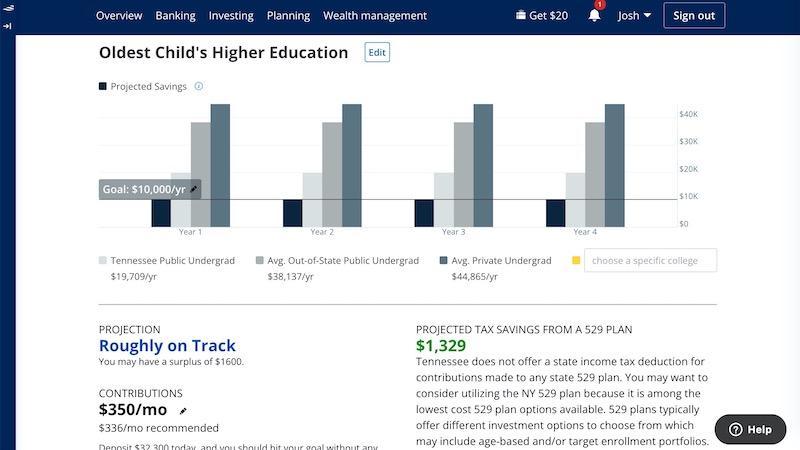

When planning for school bills, Empower Retirement Planner shows the typical annual tuition prices for in-state undergraduate, out-of-state, non-public universities, and an establishment of your alternative.

Begin by coming into your anticipated annual contribution quantity throughout your baby’s school training, plus how a lot is saved up to now. These numbers estimate how a lot it’s good to save every month to succeed in this explicit financial savings objective throughout your baby’s adolescence.

This train helps decide in the event you can afford these life occasions and retirement. For instance, I presently should contribute much less to the school fund to keep away from detrimental money move in retirement.

Should you’re beginning your parenting journey or will likely be quickly, operating these calculations years upfront gives loads of time to regulate and obtain a fascinating retirement portfolio worth.

As a aspect profit, the planner additionally estimates your potential tax financial savings from 529 contributions. It seems to be for different methods to optimize your money investments, too.

Make a Retirement Funds

Estimating your retirement bills is pivotal. The life-style you anticipate dwelling determines how a lot it’s good to save and the way shortly you’ll be able to draw down your stability.

A number of modifications are afoot as you cease incomes a full-time earnings however change to Social Safety and your investments to pay the payments. You might also turn out to be eligible for Medicare at age 65 and should navigate altering healthcare premiums.

Your retirement funds ought to embrace the next:

- Core month-to-month bills: Meals, utilities, insurance coverage, transportation, and housing.

- Healthcare: Pre-Medicare well being protection, Medicare dietary supplements, and many others.

- Journey: Holidays and visiting household or buddies.

- Social Safety: Your estimated annual advantages are based mostly in your beginning age.

- Different earnings: Wage from a part-time job, pensions, annuities, and funding properties.

You could have to account for a protection hole between your retirement age and when Social Safety and Medicare advantages kick in. Your projections could point out a large drop in your projected portfolio stability earlier than rebounding as soon as your advantages begin.

Run a number of eventualities to discover a sensible retirement age and earnings funds.

Maximize Tax-Advantaged Retirement Accounts

Conventional and Roth retirement accounts could be the inspiration of life financial savings, so that you’re not relying totally on Social Safety. Specifically, your contributions are tax-advantaged as you solely pay taxes as soon as.

Office accounts resembling 401(okay), 403(b), and Thrift Financial savings Plan (TSP) have excessive annual contribution limits, and your employer may match a specific amount. Fewer employers supply pension plans, making these contributions extra helpful than earlier than.

Particular person retirement accounts (IRAs) additionally play a task in order for you further monetary flexibility or in case your present employer doesn’t supply retirement advantages. You possibly can concurrently contribute to IRAs and employer-sponsored plans to extend your retirement reserves.

Among the greatest practices embrace:

- Recurring contributions: Automating your contributions to offer your portfolio essentially the most alternative to speculate new cash and earn compound curiosity.

- Catch-up contributions: You can also make further retirement account “catch-up contributions” beginning at age 55. Use this perk to seize extra tax-friendly beneficial properties or to assist offset a forecasted money move scarcity.

- Diversification: A correct allocation on your age and threat tolerance helps guarantee you aren’t too aggressive or conservative. Place sizing additionally manages threat to optimize your funding returns in bullish or bearish market cycles.

- Tax effectivity: Sure income-producing property are a greater match for tax-advantaged accounts to cut back your lifetime tax burden. Additional, resolve if the normal tax-deferred or Roth tax-free therapy is best on your retirement funds.

Syncing your accounts with Empower permits you to observe your portfolio efficiency and real-time worth. Routine Retirement Planner check-ins make it easier to decide whether or not you’re nonetheless on observe.

Routine Funding Checkups

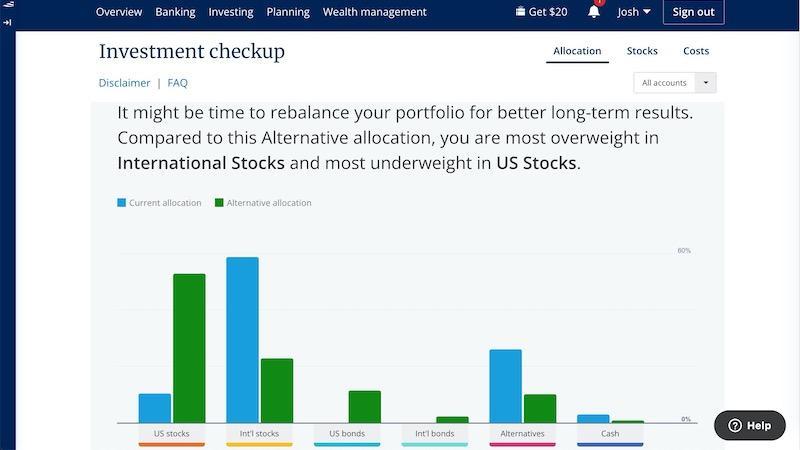

Establishing your retirement portfolio is simply step one to reaching your goal stability. You need to recurrently assessment your asset allocation to make sure you stay adequately diversified on your age and threat tolerance.

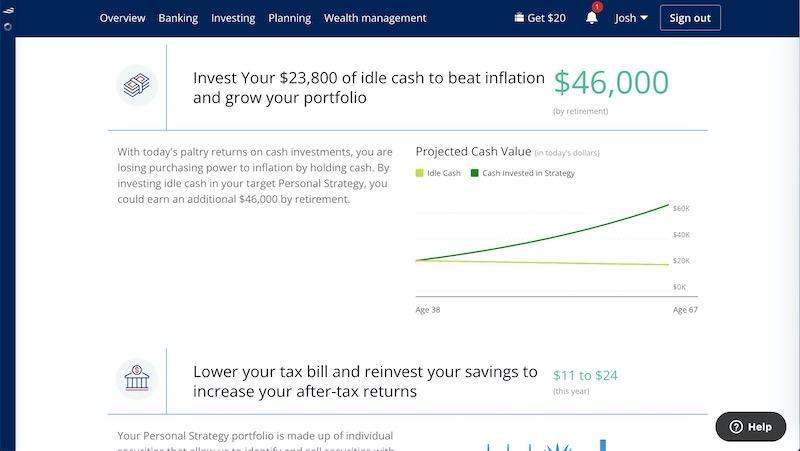

Empower gives on-demand checkups highlighting your present allocations and another allocation that may optimize your potential returns and cut back your portfolio threat. Due to its degree of element, it’s certainly one of my favourite free portfolio evaluation instruments for routine rebalancing.

Particularly, you’ll be able to view the historic returns and threat on your present allocation and various portfolios. Additional, you will note which asset lessons you could have essentially the most and least publicity to and may consider first throughout your subsequent rebalance.

You could have an excessive amount of publicity to home shares and should profit from extra worldwide inventory funds. Whereas much less thrilling, it could be time so as to add extra bonds to your portfolio for stability and earnings.

The checkup goes additional by offering a exact greenback quantity to extend or lower your property to realize an excellent stability. Not each investing app gives comparable insights, and having an additional set of eyes in your portfolio could be priceless.

Your various allocation percentages are based mostly on a number of questions you reply in your funding profile. You possibly can periodically re-answer this questionnaire for an correct evaluation as your profession and financial savings habits progress.

The planner backtests your portfolio in opposition to funding returns courting again to 1992. Whereas historic efficiency doesn’t foretell future outcomes, incorporating 30 years of bullish and bearish market cycles is a wonderful indicator.

Analyze Retirement Charges

Funding charges are simple to miss and focus virtually totally on potential funding efficiency and portfolio diversification. Nonetheless, the continued prices of pricy funds or excessive 401(okay) administration charges can considerably damper your lifetime earnings.

Whereas retirement plan suppliers should disclose all relevant charges, the quantities could appear trivial in comparison with your contribution quantities and potential development. Moreover, many employees are merely unaware of the charge quantities and their potential implications.

Your retirement plans can embrace the next charges:

- Funding charges: Mutual fund and ETF expense ratios, buying and selling commissions, and many others.

- Plan charges: Administrative charges, recordkeeping bills, and many others.

- Service charges: Non-obligatory providers resembling loans and advisory providers.

Many charges are percentage-based, so your prices enhance as your portfolio stability expands. Annual plan administration charges and buying and selling commissions are normally a hard and fast greenback quantity.

Empower Retirement Planner estimates your lifetime charges by analyzing your present portfolio, contribution quantities, and account bills. It additionally calculates annual charges by funding in your synced employer-sponsored accounts and IRAs.

Most people pay roughly 1% in annual 401(okay) charges. This step helps you assess your present plan and determine areas for enchancment.

Relying in your 401(okay) funding choices, you’ll be able to change from actively managed funds to low-cost index funds or target-date funds whereas sustaining a diversified portfolio similar to your objectives.

If in case you have a awful 401(okay) plan, a typical technique is contributing sufficient to earn your employer’s match and make investments the rest of your retirement financial savings in particular person accounts. Your private IRA will seemingly be fee-free and have low-cost funding selections.

Make Enhancements

The planner’s simulations use your beginning portfolio stability and objectives to recommend enhancements that bolster your fast and retirement funds. These insightful options assist you already know the place to focus with particular motion steps.

The modifications could be simple to implement relying in your objectives and funds. Working a number of prospects additionally helps you see when you’ll be able to attain monetary independence.

The ideas could make it easier to:

- Enhance your asset allocation

- Enhance your retirement stability

- Cut back tax legal responsibility

If that is the primary time analyzing your retirement technique, the following tips could be helpful and supply peace of thoughts.

Ultimate Ideas

The Empower Retirement Planner makes retirement planning simple, as you’ll be able to shortly view your progress, add objectives, and make corresponding modifications.

You may also free-run a number of eventualities and simulations to get peace of thoughts.