{kind=link}

December 9, 2025

Prices occur. And worth will increase on all the things could possibly be probably the most life-impacting growth of 2025.

Prices occur. And worth will increase on all the things could possibly be probably the most life-impacting growth of 2025. Trying forward, tens of millions of persons are anticipated to determine that medical health insurance is unaffordable for them in 2026 — they usually’ll doubtless cancel their well being protection.

However medical health insurance will not be the one strategy to pay for healthcare. Many individuals are uninsured and face out-of-pocket healthcare prices. They’re generally known as cash-pay clients. This selection may be daunting for individuals with critical circumstances resembling most cancers, however there are methods to efficiently navigate prices with out medical health insurance whereas avoiding medical debt.

GoodRx, a platform for medicine financial savings, shares how one can deal with your healthcare prices when you drop your insurance coverage for the 2026 protection yr.

Key takeaways:

- For the 2026 protection yr, each medical health insurance choice obtainable to you could be unaffordable.

- Whether or not you usually have a well being plan or your protection is sporadic — however you had medical health insurance in 2025 — you could decide to turn into a cash-pay healthcare client in 2026.

- For those who can’t afford insurance coverage or determine to go and not using a plan for 2026, you’ve got many healthcare choices.

What are your choices for healthcare with out insurance coverage?

Within the U.S., most individuals have medical health insurance. This protection comes by way of Medicaid, Medicare, or particular person and household plans provided by employers. In 2025, greater than 24 million individuals have been lined by a plan provided on the Inexpensive Care Act (ACA) market. However enrollment is anticipated to plummet if the income-based ACA premium subsidies (often known as premium tax credit) aren’t continued on the similar ranges in 2026. These subsidies are what made plans reasonably priced for about 22 million individuals in 2025.

Healthcare choices that don’t contain insurance coverage

For those who can’t afford medical health insurance in 2026 — otherwise you’ve determined to drop protection for any purpose — listed here are some self-pay healthcare choices you would possibly use.

- Direct main care: Direct main care (DPC) is another healthcare mannequin for accessing medical care with out insurance coverage. You make the care and cost preparations with a healthcare skilled and pay out of pocket. DPC could also be provided by a doctor, a doctor affiliate (PA, often known as a doctor assistant), or a complicated follow nurse, resembling a nurse practitioner. Your DPC association usually covers routine care, administration of power circumstances, acute-care visits, and care coordination. Emergency and hospital companies aren’t included.

- Money-pay care with religion estimate: For those who’re not utilizing insurance coverage to pay in your care, you’re entitled to a good religion estimate (GFE), which is an itemized listing of anticipated prices for a scheduled service. In case your invoice is $400 or greater than the GFE, you may dispute the invoice.

- Concierge care: Concierge care is a membership-based mannequin, usually with an annual retainer payment that provides you direct entry to a doctor. Identical-day appointments are normally obtainable. Concierge care workplaces usually restrict the variety of sufferers and provide longer appointments than a typical follow. Concierge care usually attracts higher-income customers and may be referred to as concierge drugs, retainer-based drugs, a platinum follow, or boutique drugs.

- Medical cost-sharing: Generally referred to as healthcare sharing plans, these applications are communal fashions during which group members pool their cash to cowl one another’s accredited medical prices. Medical cost-sharing applications aren’t insurance coverage, and member prices is probably not paid. There are monetary dangers, and members can find yourself with unpaid payments, resulting in hefty medical debt.

- Saving your premiums to pay for care: Many individuals have been paying a whole bunch of {dollars} month-to-month for medical health insurance premiums. What if, only for 2026, you redirected that money to a financial savings account and used the funds to pay immediately for healthcare? Healthcare amenities and hospital methods are signaling that extra persons are cash-pay clients. More and more, affected person kinds and healthcare skilled search instruments are providing particular steerage for self-pay and uninsured customers.

- Tax-advantaged healthcare accounts: Your office could provide a well being reimbursement association (HRA) in lieu of medical health insurance. (You too can have an HRA with medical health insurance or use the funds to pay premiums for a plan you purchase your self.) Solely your employer contributes to an HRA. You usually don’t should pay state or federal taxes on the cash reimbursed to you from the account for certified healthcare bills. If provided by your employer, you may as well have a versatile spending account (FSA) with out enrollment in a well being plan.

- Money care: There are healthcare amenities and different comfort areas which have clear and/or flat-free pricing for companies, resembling retail clinics — usually present in pharmacies or grocery shops — and pressing care facilities.

- Sliding-scale care: Care at group clinics is usually low value, however not free. There are additionally free and low-cost healthcare choices obtainable nationwide.

- Affected person help applications: For those who don’t have insurance coverage, you may qualify without spending a dime healthcare and prescription drugs from affected person help applications.

- Charity care: Also called indigent care, you could qualify if you’re medically indigent. This implies medical payments make up a major share of your earnings, and medical debt threatens your monetary stability. You’re financially indigent whenever you’re uninsured or underinsured, and your family earnings falls beneath a sure threshold. Nonprofit hospitals are legally required to supply any such monetary help, and a few for-profit hospitals do, too.

What concerning the ACA premium subsidies?

As of Dec. 5, 2025, ACA premium subsidies haven’t been accredited for the 2026 protection yr. The query about whether or not these premium tax credit will proceed has enormously impacted the open enrollment season. Despite the fact that the 43-day federal authorities shutdown ended on Nov. 12, 2025, the White Home and Congress proceed to barter about these healthcare subsidies.

With out the subsidies, premiums are anticipated to double, on common, in 2026. In the event that they disappear, meaning individuals with ACA plans should cowl the complete charge for his or her insurance coverage. Many individuals who rely on these reductions to afford well being plans haven’t enrolled in plans or renewed protection for 2026 on the federal and state marketplaces.

As well as, premiums are spiking in 2026 for Medicare Half B in addition to for a lot of Medicare Benefit and employer-based plans.

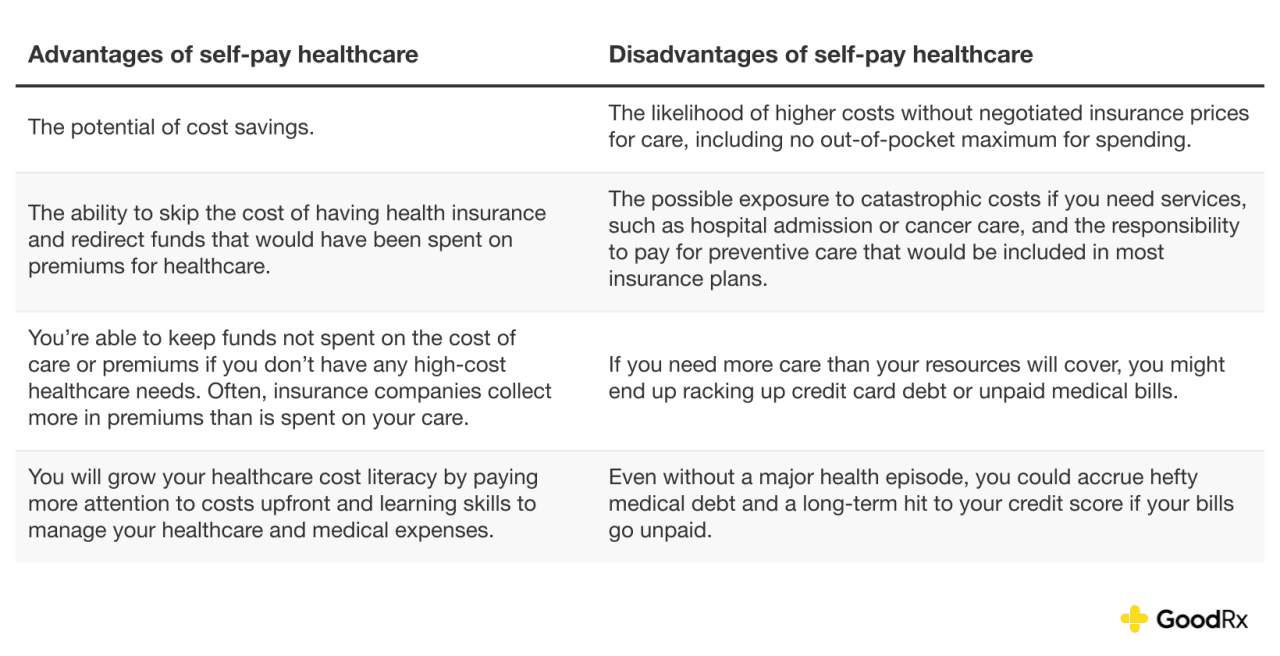

Professionals and cons of self-pay healthcare

There are benefits and drawbacks of self-pay healthcare. It may be more cost effective, however not all the time. You probably have even reasonable well being issues, it’s hardly ever more cost effective — particularly when you develop an surprising well being situation. Earlier than deciding to go this route, you might also need to think about choices for accessing healthcare with out insurance coverage, resembling:

- Money-pay amenities close to you.

- Having a technique for evaluating prices.

- Having the assets to pay for the healthcare — together with prescriptions — that you simply or your loved ones members might have, whereas weighing the truth that not having insurance coverage can expose you to large medical debt.

Right here’s a snapshot of some constructive points of skipping insurance coverage versus why dropping protection may not be a good suggestion for you and your loved ones.

Professionals and cons of self-pay healthcare

Who would possibly be capable of danger going uninsured?

Missing insurance coverage has dangers, together with medical debt — which might lead you to medical chapter. However being uninsured can also be widespread. In 2023, an estimated 8% of the U.S. inhabitants lacked insurance coverage, and greater than 9% of individuals ages 0 to 64 have been uninsured.

It’s necessary to notice that selecting a yr or extra of cash-pay care will not be ideally suited for most individuals. Those that would possibly danger the least by selecting self-pay healthcare embody:

- Wholesome individuals who don’t have power circumstances.

- Younger individuals.

- People who find themselves not liable to accidents.

- Individuals with greater incomes.

- Individuals who plan to enroll in insurance coverage the next yr (or sooner).

Why would you need to drop your medical health insurance?

Usually, individuals don’t need to drop medical health insurance, however circumstances — mainly value — are why they will not proceed with a plan. The reason why you could need to drop your medical health insurance embody a number of of the next:

- Premiums are unaffordable.

- The deductible is simply too expensive in your price range.

- ACA subsidies may not be provided in 2026.

- The protection doesn’t meet your wants.

- The prescription protection doesn’t embody the drugs you’re taking.

- You will have entry to a different well being plan that meets your wants and/or prices much less.

- You progress out of the protection space.

cancel medical health insurance

You’ll be able to cancel your medical health insurance by contacting your plan, or when you (or your employer) are not paying premiums. Right here’s easy methods to cancel your protection:

- Decide whether or not you’re stopping protection only for your self or for everybody lined by your plan. That is particularly necessary if you’re canceling COBRA medical health insurance.

- Decide what protection you need to cease. It’s possible you’ll need to drop a complete healthcare plan, prescription protection solely, dental protection solely, or only a imaginative and prescient plan.

- Decide whether or not you may cancel protection. You probably have an worker or group plan, you usually must have a qualifying life occasion (QLE) or go away your employment to cancel protection. You probably have a Medicare Benefit plan, you may drop protection in the course of the Medicare open enrollment interval, the Medicare Benefit open enrollment interval, or when you qualify for a particular enrollment interval (SEP). You’ll be able to disenroll from a standalone Medicare Half D plan throughout Medicare open enrollment, when you’ve got a standalone Half D plan and a Medicare Benefit plan, or when you qualify for an SEP.

- You probably have an ACA market plan, you may contact the nationwide or state market that offered your plan — or the insurance coverage firm. You too can log into your market account and cancel.

- A medical health insurance plan may be canceled by the insurance coverage firm when you fail to pay the premium.

- For those who don’t join medical health insurance throughout your open enrollment interval — or take no matter motion indicators you need to drop your insurance coverage for 2026 — you’ll cancel your protection.

Is there a penalty for canceling medical health insurance?

A nationwide mandate set after the ACA regulation handed in 2010 was eradicated in 2019. You possibly can face a requirement (some with a monetary penalty) for not having medical health insurance when you reside in sure states or Washington, D.C.

- California: Residents have a penalty for not having protection, however the quantity varies yearly. For the 2024 tax yr, the penalty was no less than $900 per grownup and $450 per dependent beneath 18 in a family. (That is probably the most present info obtainable on the time of publication.) Residents can use the state’s Particular person Shared Duty Penalty Estimator to find out the potential quantity owed for the present tax yr.

- Massachusetts: The Massachusetts healthcare particular person mandate doesn’t apply to anybody beneath the age of 18. It additionally doesn’t apply to individuals with a professional hardship or an exemption and people whose incomes are equal to or lower than 150% of the federal poverty stage (FPL). The penalty is assessed on a sliding scale. As an example, for the 2025 tax yr, people with out insurance coverage should pay $300 per yr in the event that they earn 150.1% to 200% of the FPL and $588 per yr in the event that they earn 200.1% to 250% of the FPL.

- New Jersey: The New Jersey Shared Duty Requirement is assessed primarily based on what number of months individuals within the family didn’t have minimal important protection or a protection exemption. For the 2025 tax yr, the quantity ranges from $695 to $4,908 for a person taxpayer and will increase primarily based on the variety of extra uninsured individuals within the family in addition to family earnings.

- Rhode Island: The RI Well being Insurance coverage Mandate is whichever of those quantities is bigger: 2.5% of annual family earnings or $695 per grownup and $347.50 per dependent beneath 18.

- Washington, D.C.: The Particular person Duty Requirement for anybody who goes with out protection for all of 2025 is the higher of: 2.5% of annual family earnings over the federal tax submitting threshold, or $795 per grownup and $397.50 per dependent beneath 18, with a cap of $2,385 per household.

- Vermont: There may be no monetary penalty, however residents should report whether or not they have medical health insurance once they file their state taxes.

- Maryland: Residents are requested about medical health insurance standing once they file state taxes as an avenue to enrollment.

The underside line

Medical insurance will not be the one strategy to cowl healthcare prices. Individuals who entry healthcare with out insurance coverage are generally known as cash-pay clients. This is usually a difficult choice for individuals with power circumstances or very expensive care, resembling for most cancers. However there are methods to efficiently deal with the prices of healthcare with out insurance coverage whereas sidestepping hefty medical debt.

Choices used alone or together embody: direct main care, money clinics, tax-advantaged healthcare accounts, sliding-scale care, affected person help applications, and hospital charity care. Many individuals will determine whether or not to cancel medical health insurance in 2026 primarily based on whether or not the Inexpensive Care Act (ACA) marketplaces have premium subsidies obtainable.

This story was produced by GoodRx and reviewed and distributed by Stacker.

RELATED CONTENT: Prairie View A&M College Launches Program To Assist College students With Sickle Cell Illness